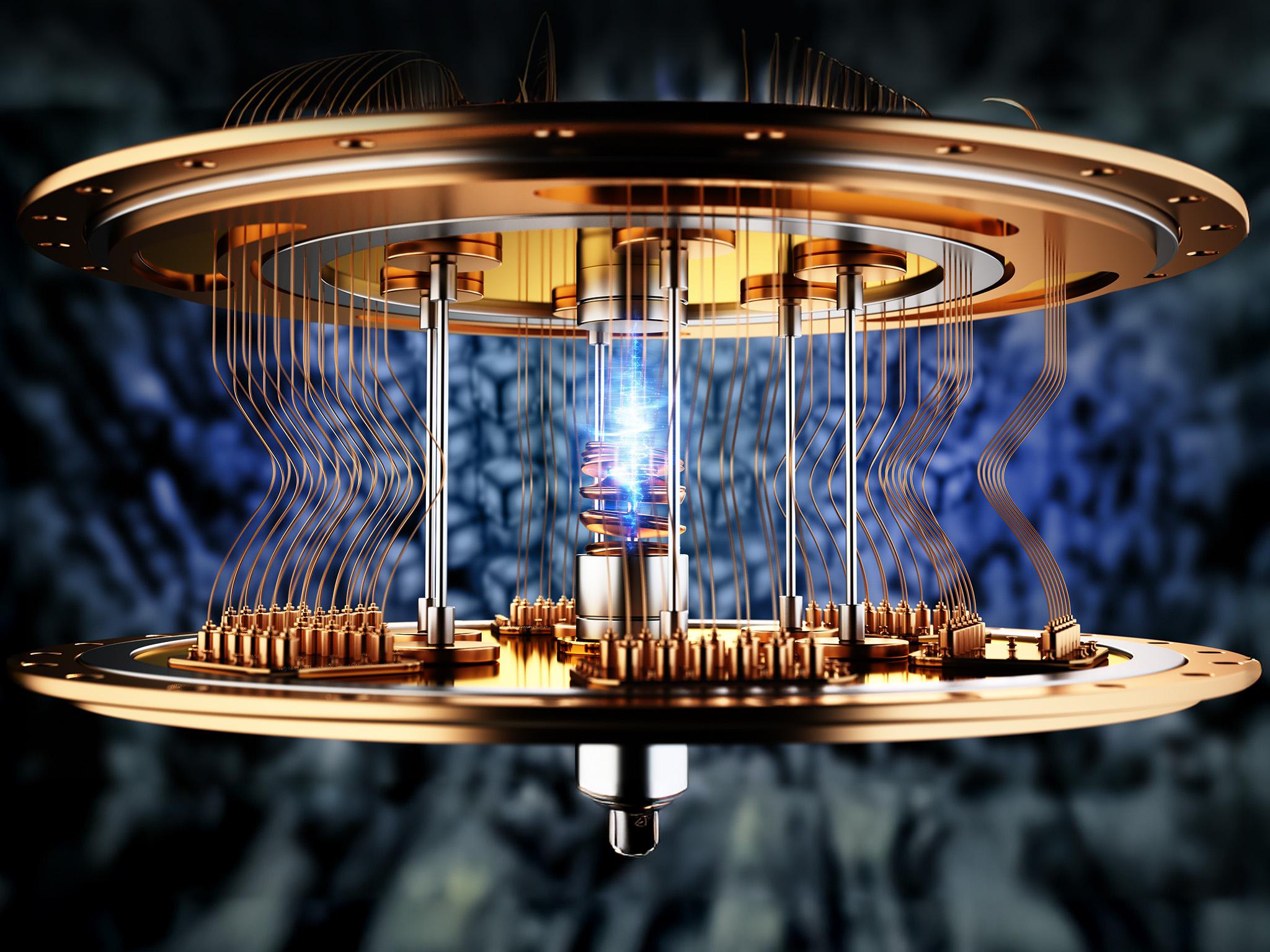

The competitive landscape of the global quantum computing industry is a unique and dynamic ecosystem, characterized by a mix of established technology behemoths, specialized pure-play hardware startups, and a burgeoning software and services sector. A competitive analysis of the Quantum Computing Market reveals that the hardware development space is currently led by a handful of the world's largest technology companies. Google and IBM have been at the forefront of the superconducting qubit approach, engaging in a well-publicized race to build processors with an increasing number of higher-quality qubits. Their strategy involves leveraging their immense R&D budgets and deep expertise in physics and engineering to push the fundamental science forward, while also building a cloud platform around their hardware to foster a developer community. Microsoft is pursuing a more long-term and high-risk, high-reward strategy with its focus on developing topological qubits, which are theoretically much more stable and resistant to errors, though they have yet to be experimentally demonstrated. These tech giants are all pursuing a full-stack approach, aiming to control the hardware, the software, and the cloud access layer.

Complementing the efforts of the tech giants is a vibrant and well-funded ecosystem of specialized, venture-backed startups that are often pioneers in alternative hardware modalities. IonQ, for example, has established itself as a commercial leader in the trapped-ion approach and was the first pure-play quantum computing hardware company to become publicly traded. Quantinuum, the result of a merger between Honeywell's quantum division and a software company, is another major player in the trapped-ion space, pursuing a strategy of vertical integration that combines high-fidelity hardware with advanced quantum software. In the photonic quantum computing realm, startups like PsiQuantum and Xanadu are pursuing a fundamentally different path that promises room-temperature operation and scalability through semiconductor manufacturing. Other notable startups like Rigetti Computing (superconducting) and Atom Computing (neutral atoms) are also making significant technical progress. The competitive strategy for these pure-play companies is to achieve a technical breakthrough in their chosen modality that demonstrates a clear advantage in terms of qubit quality, scale, or cost, which would allow them to out-compete the more diversified efforts of the larger players.

The competitive landscape is not limited to hardware. A crucial and rapidly growing segment of the market is focused on quantum software, algorithms, and applications. This includes companies that are developing quantum software development kits (SDKs) and compilers that act as the "middleware" between a user's algorithm and the physical quantum hardware. It also includes a new generation of startups that are focused on building quantum-inspired or quantum-ready applications for specific industry verticals, such as finance or pharmaceuticals, without necessarily building their own hardware. These companies often operate on a hardware-agnostic basis, developing software that can run on multiple different quantum cloud platforms. The major cloud providers themselves—Amazon with Braket, Microsoft with Azure Quantum, and IBM with its Quantum Experience—are also key players, acting as aggregators and distributors. They provide cloud-based access to a variety of different quantum hardware backends (from both their own labs and their startup partners), effectively creating a marketplace for quantum computation. The Quantum Computing Market size is projected to grow USD 14.19 Billion by 2035, exhibiting a CAGR of 27.04% during the forecast period 2025-2035.

Top Trending Reports -