As the demand for energy-efficient solutions continues to soar, the silicon carbide (SiC) power devices segment is set to exceed expectations, with projections indicating a staggering growth to USD 50.1 billion by 2035. According to Market Research Future, this market is experiencing a compound annual growth rate (CAGR) of 23.4%, driven by a plethora of factors including the electrification of the automotive sector and increasing renewable energy deployments. The push for high efficiency power electronics is particularly evident as sectors like electric vehicles (EVs) embrace SiC technology for its superior performance and efficiency. With the current market size estimated at USD 2.7 billion in 2024, the trajectory for silicon carbide power devices is both promising and transformative.

The SiC Power Semiconductor Market has gained momentum, especially in key regions such as North America, which currently leads in revenue generation. The adoption of SiC MOSFET technology is particularly pronounced here, with electric vehicle manufacturers recognizing the advantages of these high voltage semiconductor devices. Major companies contributing to the market's dynamism include Wolfspeed (US), Infineon Technologies (DE), and ON Semiconductor (US). These enterprises are pivotal in advancing the innovation landscape, enabling faster, more efficient power management solutions. Moreover, the Asia-Pacific region is emerging as the fastest-growing market, catalyzed by its robust manufacturing capabilities and technological advancements in power electronics.

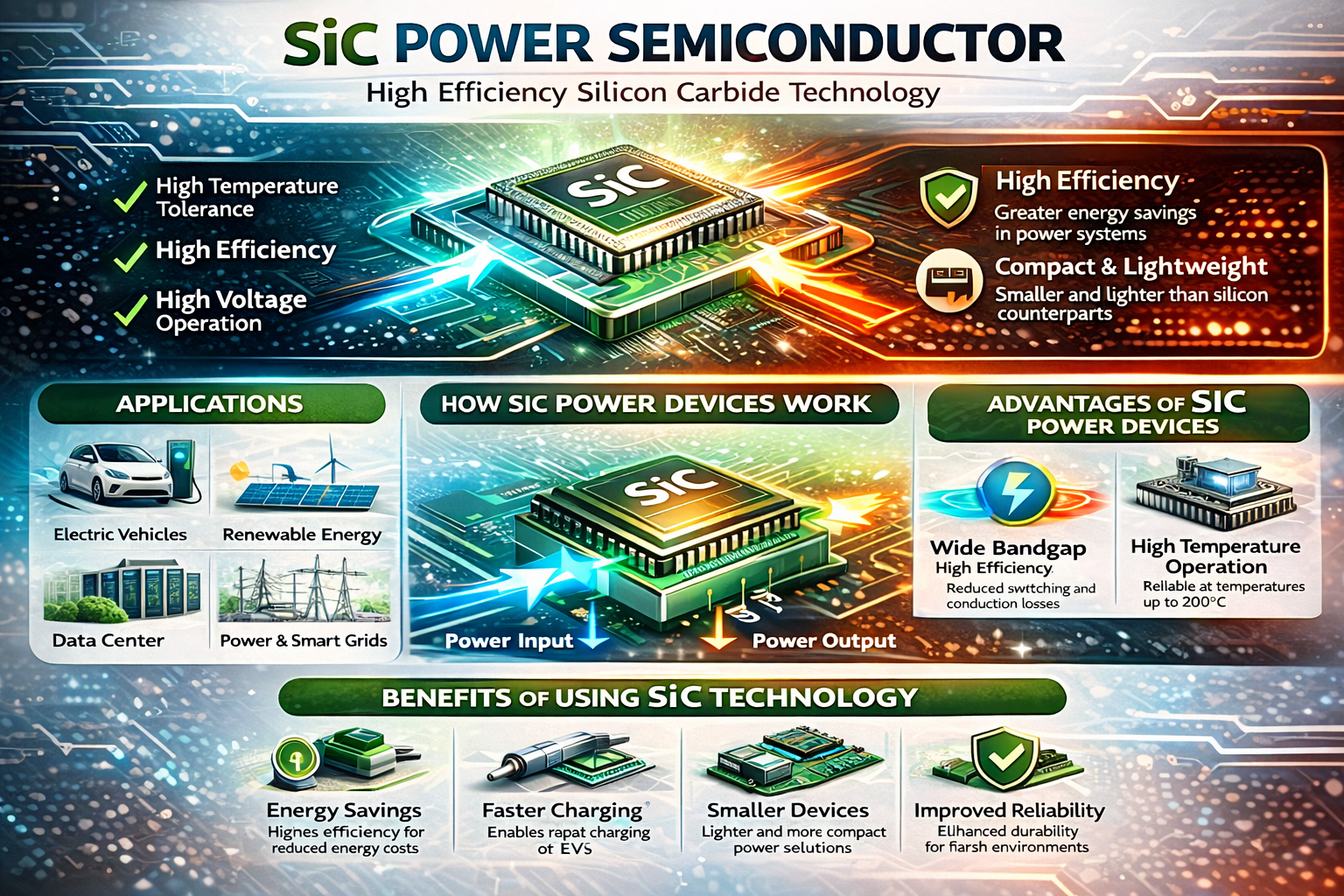

Several driving forces are contributing to the enhanced market demand for silicon carbide power devices. The rising adoption of electric vehicles is a primary catalyst, enhancing the need for high efficiency power electronics that improve vehicle performance and energy retention. Furthermore, the shift towards renewable energy sources, such as solar and wind power, necessitates power electronics that handle higher voltages and deliver improved efficiency. With SiC technology, manufacturers can achieve better thermal management and reduced energy losses, thereby meeting stringent regulatory standards for emissions and energy consumption. However, challenges such as the high cost of manufacturing SiC substrates compared to traditional silicon devices pose potential barriers to widespread adoption. Nonetheless, the long-term operational savings and efficiency offered by SiC devices are projected to outweigh initial investments, propelling their integration across various applications.

North America stands as a frontrunner in the silicon carbide power devices market, largely due to the region's aggressive adoption of electric vehicles and government incentives aimed at promoting sustainable technologies. The increasing presence of key players like Cree (US) and Texas Instruments (US) bolsters the region's competitive edge, fostering innovations that align with market demands. On the other hand, the Asia-Pacific region is not far behind, with countries like Japan and China investing heavily in high efficiency power electronics. The growth in this region is largely attributed to advancements in manufacturing methodologies, which enable firms like ROHM Semiconductor (JP) and Mitsubishi Electric (JP) to scale production and meet burgeoning international demand. The development of SiC Power Semiconductor Market continues to influence strategic direction within the sector.

The landscape for silicon carbide power devices is rife with opportunities, particularly as the global shift towards sustainable energy continues. The growing demand for high voltage semiconductor devices provides an avenue for innovative solutions that enhance efficiency. Specific opportunities include the integration of SiC power devices in renewable energy systems and electric vehicle powertrains, which are expected to lead to significant reductions in energy consumption and emissions. Furthermore, the emergence of SiC bare die devices as a fast-growing segment highlights a shift in market dynamics, as these components offer flexible integration across various applications. The sustained focus on reducing carbon footprints further augments the market potential, pushing manufacturers to enhance their production capabilities and technological advancements.

In 2022, it was noted that the global electric vehicle market reached a valuation of USD 162.3 billion, with projections suggesting it could surpass USD 800 billion by 2027. This rapid growth correlates with the increasing implementation of SiC power devices, which facilitate more efficient energy conversion and management in EVs. For instance, Tesla's integration of SiC MOSFETs in its power electronics has resulted in a 20% increase in driving range compared to previous models using conventional silicon technologies. Moreover, as renewable energy generation is expected to exceed 50% of the global electricity mix by 2030, the demand for high-efficiency SiC devices capable of managing the higher voltages associated with solar inverters and wind turbines will likely rise significantly. This creates a feedback loop where increased renewable energy deployment necessitates more SiC devices, further driving market growth.

As we move closer to 2035, the outlook for the silicon carbide power devices market remains robust. Analysts anticipate that continued technological advancements will pave the way for innovative applications in sectors like telecommunications and industrial automation, expanding the market's reach. Investment in research and development will be crucial in overcoming existing challenges related to manufacturing costs and performance optimization. The cumulative effects of these advancements are expected to significantly alter the competitive landscape, providing early adopters with a critical advantage in efficiency and operational cost savings.

AI Impact Analysis

The integration of artificial intelligence (AI) and machine learning (ML) technologies is projected to revolutionize the silicon carbide power devices market. AI-driven analytics can optimize manufacturing processes, ensuring higher yields and reduced waste during the production of silicon carbide substrates. Additionally, organizations can leverage AI for predictive maintenance in power electronics systems, significantly enhancing reliability and uptime. The convergence of AI with high efficiency power electronics will also facilitate smarter energy management systems, optimizing energy distribution and consumption across various sectors.